The Gap Between A Sale And A Stall Is Rarely Price

Introduction

Ray has run his precision-engineering business in the West Midlands for thirty-one years. Revenue is around £14m, profit before the add-backs is healthy, and the order book is full. When a buy-and-build acquirer's email landed in March, he allowed himself to picture the end of it: the handover, the cheque, the boat he has talked about for a decade.

Six weeks later the conversation has gone quiet. The buyer was complimentary about the engineering and the people, then asked for three years of management accounts by product line, the terms of the contract with his largest customer, and a note on what happens to the business when Ray is not in the building. None of those things exist in the form the buyer wants. The deal has not died. It has stalled — and a stall, in this market, is how most quiet rejections begin.

Ray's business is good. That is precisely the problem worth understanding, because good is no longer the same as sellable.

1) The Market Is Open — But Only For The Prepared

The UK lower mid-market has moved out of last year's pre-Budget caution into a more active phase. But the recovery is uneven, and the unevenness is the whole story. Across the market as a whole, deal volume has fallen by roughly 12% over the past year while total deal values have risen by around 12% and the average deal size has climbed by close to 28%. Fewer transactions, larger and higher-quality ones: capital is concentrating on the best assets.

In the lower mid-market the same pattern shows up as a two-speed market. Volume has not expanded as quickly as value, and buyers are intensely focused on earnings quality. Well-prepared, premium businesses attract competitive bidding. Average or under-prepared ones sit on the shelf — looked at, complimented, and left.

That is the trap Ray is walking into. He assumed a full order book and a long history would carry the day. In a flight-to-quality market, they get him a first meeting. What converts the meeting into an offer is everything underneath.

Action step: Before you respond to any approach, write down the three things a buyer is most likely to probe in your business. If you cannot answer each with a document rather than a sentence, you are not ready to be in the room yet.

2) What “Quality” Means Through A Buyer's Eyes

A buyer is not paying for what the business earned. They are paying for what they believe it will keep earning after you have gone. Quality, in that sense, is a measure of risk, not ambition. Valuation in this market increasingly reflects how defensible the earnings are — repeatable, low-risk profit commands a premium, while profit that looks fragile is discounted hard or declined.

For a manufacturer, the buyer's lens settles on a familiar set of questions. How concentrated is the customer base — and what happens if the largest account leaves? Is the order book contracted or merely hoped for? Are margins stable, or do they swing with input costs and one-off jobs? What condition is the plant in, and what capital expenditure is the buyer inheriting? How dependent is output on a handful of skilled people who could retire or walk?

Ray's largest customer is about 40% of revenue, on a relationship rather than a contract. To him, that is loyalty earned over twenty years. To a buyer, it is a single point of failure that could halve the business overnight.

🚩 Diligence Flag: “The handshake contract.” A buyer will treat any major customer without a written, assignable contract as revenue at risk, and price accordingly — or hold it back in an earn-out so you carry the risk, not them. Before you go to market, get your key relationships onto contracts that survive a change of ownership. It is the single cheapest piece of value protection most founders never do.

Action step: Map your revenue by customer and ask of each: is it contracted, is the contract assignable on a sale, and how long does it run? Fix the top three exposures first.

3) The Founder-Dependency Trap

The hardest question Ray was asked is the one with no document behind it: what happens to the business when you are not there?

Buyers are placing growing weight on management depth beyond the founder. A business that depends on one individual reads as high-risk; one with an empowered team and defined reporting structures reads as lower-risk and more scalable. The logic is simple. If the company only works because the owner holds the customers, the pricing, the supplier relationships and the production know-how in his head, then the buyer is not acquiring a business. They are acquiring a job, and the one person who can do it is leaving.

This is the value driver founders find most uncomfortable, because the very habits that built the business — being across everything, being the final word — are the habits that now cap its price.

Founder Insight: “The business that needs me is worth less than the business that doesn't.” It feels like a contradiction after decades of being indispensable. But every task only you can do is a discount in the buyer's model. Spend the runway making yourself replaceable, role by role, and you are not diminishing the business — you are converting it from a job into an asset someone else can own.

Action step: List the decisions and relationships that currently run through you alone. Over the next year, move each one to a named person with the authority to own it — and let buyers see the handover already working.

4) The Documentation A Buyer Expects To Find

When the acquirer asked Ray for product-line accounts and customer terms, the request was not bureaucratic. It was the first test of whether the business is diligence-ready. Buyers expect clarity on financial performance, operational resilience and credible growth drivers — and they expect to find it quickly, in order, without the founder reconstructing it from memory.

A thin or disorganised data room does two kinds of damage. It slows the process, and time is where deals lose momentum and buyers lose nerve. And it signals that other things may be just as loosely held, which invites a harder look at everything else.

For a manufacturer, diligence-readiness means financials that reconcile and split out cleanly; contracts with customers, suppliers and landlords that are current and assignable; an asset register and a realistic view of capital expenditure; up-to-date health, safety and environmental compliance; and clear records on the workforce, including who is critical and how they are retained.

🚩 Diligence Flag: “The reconstruction scramble.” If diligence is the first time anyone has pulled these documents together, the buyer sees the gaps before you do. Build the data room before you need it — twelve months early, not twelve days into a process — so the story you tell and the story the documents tell are the same story.

5) Why Rushing The Tax Deadline Can Cost More Than It Saves

There is one more pressure pushing founders like Ray toward the door before they are ready: tax. From 6 April 2026 the Capital Gains Tax rate on qualifying Business Asset Disposal Relief disposals rose to 18%, the last step in a phased increase from 10% to 14% and now to 18%. The lifetime limit stays at £1m of qualifying gains per individual.

The instinct is to hurry — to complete before any further change. It is worth keeping the number in proportion. On £1m of qualifying gain, the move from 14% to 18% is roughly £40,000 more tax. Material, certainly. But a rushed, under-prepared sale routinely costs far more than that in a lower multiple, a larger slice held back in an earn-out, or a price chipped during diligence once the gaps appear. Selling well six months later can beat selling quickly today by a wide margin.

This is a question for your tax adviser to model on your own numbers — we are not a tax practice, and the interaction of reliefs, timing and structure is theirs to advise on. The founder-side point is simpler: let the tax tail not wag the value dog. A deadline is a reason to plan, not a reason to panic.

Action step: Ask your accountant to run the net-proceeds figures under two scenarios — a sale now and a prepared sale in 12–18 months at a realistically higher multiple — so you are deciding on the number that actually reaches your account, not the headline price.

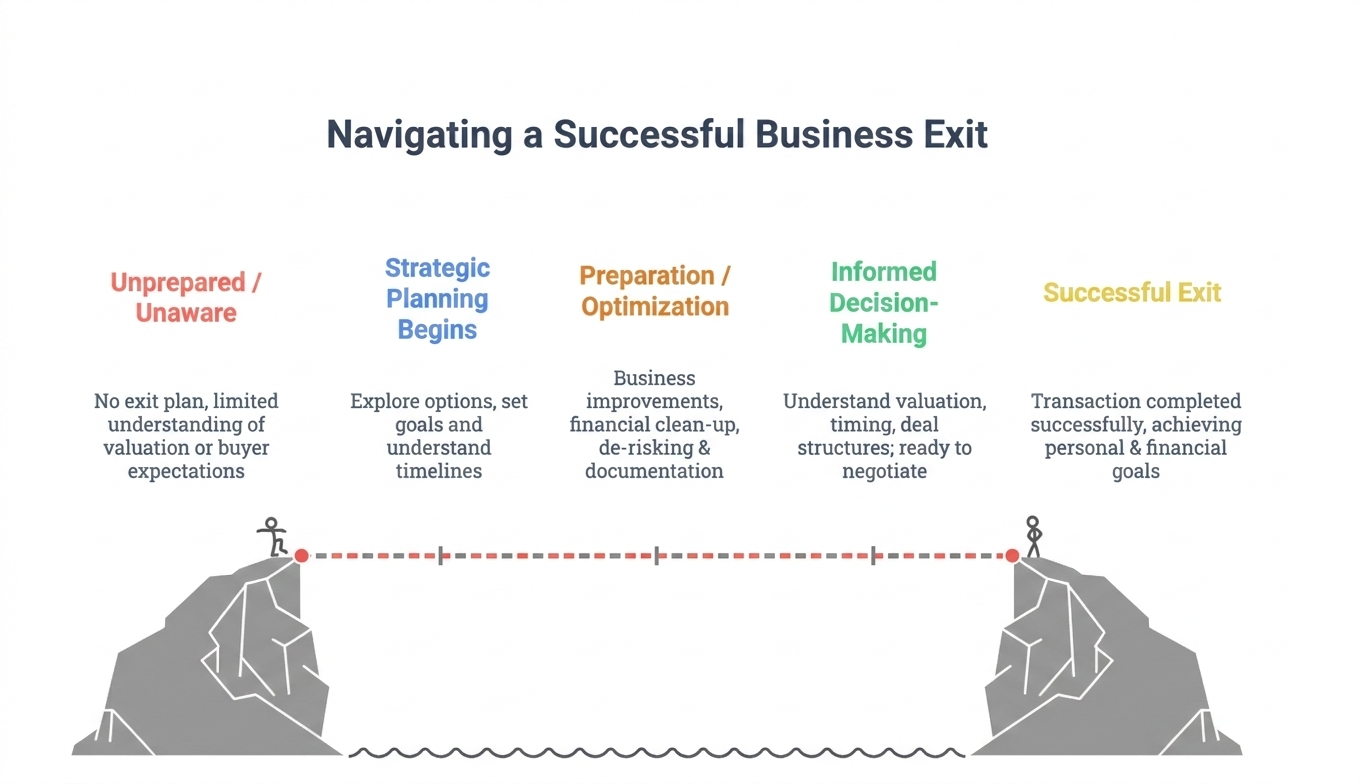

6) The Twelve-To-Twenty-Four-Month Window

The gap between Ray's business and a sellable one is not unbridgeable. It is a programme of work, and the good news is that he has time, because the approach came before he had to sell rather than after.

Used well, a 12–24 month runway is enough to move the dimensions that buyers price: spreading customer concentration and getting key relationships onto assignable contracts; building a management layer that runs the business without him; cleaning up the financials so they tell a clear, defensible story; and assembling the data room ahead of need. None of it is glamorous. All of it shows up in the multiple, and in how much of the price is paid on day one rather than deferred.

The founders who command premiums in this market are not lucky. They prepared for it — quietly, deliberately, in the period before anyone was watching.

From Shelf-Ready To Sale-Ready

Ray's story is the common one: a genuinely good business, brought to market — or to an approach — before it was ready to withstand a buyer's scrutiny. In a market sorting hard between premium assets and the rest, readiness is the difference between an offer and a polite silence.

The reassuring part is that readiness is the one variable you fully control. You cannot dictate the market, the buyer pool or the tax regime. You can decide, today, to make your business one that a careful buyer looks at and sees low risk and durable value rather than a job that happens to be profitable.

That is the work we do alongside founders — founder-side, before a deal forces the pace — so that when you choose to sell, your business is the one buyers compete for, not the one left on the shelf. If you would like to understand where yours stands today, that is exactly where an honest, buyer's-lens assessment begins.

About Exit Strategy & Solutions

Exit Strategy & Solutions is a specialist advisory firm helping UK SME owners build optionality, maximise value, and reduce risk through strategic exit planning and execution.

Our approach combines deep market intelligence, strategic positioning expertise, and an unwavering focus on protecting your interests at every stage.

Ready to explore your exit options?

Take our Exit Readiness Calculator to assess your business's exit readiness and identify opportunities to maximise valuation here: https://exitstrategyandsolutions.com/resources/calculator

Contact us:

- Email: enquiry@exitstrategyandsolutions.com

- Phone: 0330 043 4689

- Website: www.exitstrategyandsolutions.com

Disclaimer

This article is provided for informational purposes only and does not constitute legal, tax, or regulated investment advice. Examples cited are based on composite scenarios for illustrative purposes. Exit Strategy & Solutions is not responsible for decisions made based on information in this article.